HOW TO PROPERLY_

_ACCOUNT FOR

ACCRUED EXPENSES – ACCOUNT 335

“Accounting for accrued expenses in Account 335 is a crucial aspect of bookkeeping, enabling businesses to record financial obligations that have arisen during the period but have not yet been settled. A thorough understanding of the regulations related to this account, along with accurate accounting for expense items, not only ensures accuracy in financial reporting but also aids in effective cost management, while meeting legal and accounting requirements.”

CONTENT OF

THE ARTICLE

01

What is Account 335 – Accrued Exxpenses?

02

Principles of Accounting for Account 335 – Accrued Expenses and Key Considerations

03

Structure and Content Reflected in Account 335

04

Structure and Content Reflected

01

WHAT IS ACCOUNT 335 –

ACCRUED EXPENSES?

According to Circular 200/2014/TT-BTC, effective from January 1, 2015, which replaces the Corporate Accounting Regime issued under Decision No. 15/2006/QĐ-BTC dated March 20, 2006, and Circular No. 244/2009/TT-BTC dated December 31, 2009, by the Ministry of Finance

This account is used to reflect expenses payable for goods and services received from suppliers or provided to customers during the reporting period but have not been paid due to the absence of invoices or insufficient documentation. These amounts are recorded as production and business expenses for the reporting period.

Additionally, this account reflects the following types of expenses:

– Payables to employees during the period, such as accrued wages for leave days.

– Pre-accrued production and business expenses for the reporting period, including:

• Expenses during seasonal production halts, which can be planned in advance. Accountants calculate and record these anticipated costs as production and business expenses for the period.

• Pre-accrued loan interest payable in cases of deferred interest payments or bonds with deferred interest payments (e.g., upon bond maturity).

• Pre-accrued costs to temporarily estimate the cost of goods sold or real estate products already sold.

02

PRINCIPLES OF

ACCOUNTING FOR

ACCOUNT 335 – ACCRUED

EXPENSES

To present accurate financial statements in line with the nature of each item, accountants must differentiate expenses appropriately when recording them. The nature of Account 335 is defined as follows:

• Accrued expenses are current liabilities with a definite timeframe for payment.

• Accrued expenses must have a determinable amount that is certain to be paid.

• On the financial statements, accrued expenses are part of trade payables or other payables.

• Recording accrued expenses as production and business costs during the period must adhere to the matching principle, aligning revenues and expenses incurred within the same period.

* Key Notes on Principles to Follow When Accounting:

– Pre-accrued items should not be recorded in Account 335 but should be reflected as provisions for liabilities, as follows:

• Major repairs for specific fixed assets: If these repairs are periodic in nature, businesses may pre-accrue the costs for planned repairs in the following year(s);

• Warranty provisions for products, goods, construction projects, or restructuring;

• Other provisions for liabilities (as specified in Account 352).

– Pre-accrued costs for temporarily estimating the cost of products or real estate goods sold during the period must comply with additional principles:

• For costs included in the investment or construction budget but lacking sufficient documentation for acceptance testing of completed work, the company must provide a detailed explanation of the reasons and the content of the pre-accrued costs for each project item.

• For completed real estate goods identified as sold during the period and meeting the revenue recognition criteria.

• Pre-accrued costs should be estimated temporarily, and the actual incurred costs recorded as the cost of goods sold must correspond to the cost standard based on the total estimated costs for the portion of real estate goods identified as sold (calculated according to the area).

– The determination of capitalized borrowing costs must comply with the Accounting Standard on “Borrowing Costs.” Specific cases include:

• For specific loans used to construct fixed assets (FAs) or investment properties (IPs), borrowing costs can be capitalized even if the construction period is less than 12 months.

• For contractors, borrowing costs must not be capitalized when loans are used to execute construction or projects for customers, even for specific loans (e.g., a contractor borrows money to construct a building for a client)…

* Other important principles:

• Accrued expenses recorded in production and business costs during the period must be calculated rigorously (with detailed cost estimates and approval from authorized personnel) and supported by reliable evidence. Accruing expenses that cannot be classified as production or business costs is strictly prohibited.

• Accrued expenses must be reconciled with the actual incurred costs. Any difference between pre-accrued and actual expenses must be adjusted accordingly.

• Accrued expenses not used by the end of the year must be explained in the Notes to the Financial Statements.

By adhering to the accounting principles for Account 335, businesses can effectively manage cash flows, ensure that expenses are recognized in the correct period, and minimize financial risks.

STRUCTURE AND

CONTENT REFLECTED

IN ACCOUNT 335

03

04

ACCOUNTING METHODS FOR KEY ECONOMIC TRANSACTIONS

a) When accruing into expenses incurred from annual leave salary of workers, the following accounts shall be recorded as follows:

Dr 622 – Direct labor costs

Cr 335 – Accrued expenses.

b) When calculating actual annual leave salaries payable, if the accrued amount is greater than the actual expenses incurred, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (accrued amount)

Cr 622- – Direct labor costs.

c) When accruing expenses incurred from repair of fixed assets without acceptance during a period to operating expenses and issuing invoices, the following accounts shall be recorded as follows:

Dr 241, 623, 627, 641, 642.

Cr 335 – Accrued expenses.

d) When the repair of fixed assets is completed and put into operation, if the accrued amount is greater than the actual expense incurred, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (accrued amount is greater than expense incurred)

Cr 241, 623, 627, 641, 642.

dd) When accruing estimated expenses payable during seasonal or planned production cessation period into operating expenses, the following accounts shall be recorded as follows:

Dr 623 – Costs of construction machinery

Dr 627 – Factory overheads

Cr 335 – Accrued expenses.

e) Actual expenses incurring from accrued expenses, the following accounts shall be recorded as follows:

Dr 623, 627 (if the expense incurred is greater than the accrued amount)

Dr 335 – Accrued expenses (accrued amount)

Dr 133 – Deductible VAT (if any)

Cr 111, 112, 152, 153, 331, 334

Cr 623, 627 (if the expense incurred is smaller than the accrued amount)

g) When determining deferred interest payable in period at end of period, the following accounts shall be recorded as follows:

Dr 635 – Financial expenses (loans interests for business capital)

Dr 627, 241 (capitalized interests)

Cr 335 – Accrued expenses.

h) In case the enterprise issues bonds at par value, if interests are deferred (at maturity of bonds), periodically, the enterprise must accrue loan interests expenses payable in period into operating expenses, or capitalization of interests, and the following accounts shall be recorded as follows:

Dr 627, 241 (capitalized interests)

Dr 635 – Financial expenses (if the interest is included in financial expenses)

Cr 335 – Accrued expenses (bond interest payables in the period).

At the maturity of the bond, when the enterprise pays principal and interest of the bond to the bondholder, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (total bond interests)

Dr 34311 – Bond par value

Cr 111, 112, etc.

i) In case the enterprise issues bonds at discount, if interests are deferred (at maturity of bonds), periodically, enterprises must accrue loan interests expenses payable in period into operating expenses or capitalization of interests, and the following accounts shall be recorded as follows:

Dr 627, 241 (capitalized interests)

Dr 635 – Financial expenses (if the interest is included in financial expenses)

Cr 335 – Accrued expenses (bond interest payables in the period).

Cr 34312 – Bond discounts (bond discount allocated in period).

At the maturity of the bond, when the enterprise pays principal and interest of the bond to the bondholder, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (total bond interests)

Dr 34311 – Bond par value

Cr 111, 112, etc.

k) In case the enterprise issues bonds at premium, if interests are deferred (at maturity of bonds), periodically, enterprises must accrue loan interests expenses payable in period into operating expenses or capitalization of interests, and the following accounts shall be recorded as follows:

Dr 627, 241 (capitalized interests)

Dr 635 – Financial expenses (if the interest is included in financial expenses)

Cr 335 – Accrued expenses (bond interest payables in the period).

At the maturity of the bond, when the enterprise pays principal and interest of the bond to the bondholder, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (total bond interests)

Dr 34311 – Bond par value

Cr 111, 112, etc.

l) Regarding wholly-state-owned enterprises converted into joint-stock companies:

– Regarding overdue loans given by JSC Bank for Foreign Trade of Vietnam and the Vietnam Development Bank because the enterprise suffers losses, has no state capital and close to insolvency, the equitized enterprise must apply for freezing, rescheduling or cancelling debts of bank interests as prescribed in regulations of law in force. When receiving the decision of cancellation of outstanding interests, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses (cancelled interests)

Cr 421 – Undistributed profit after tax (the loan interests recorded to expenses of previous periods which are cancelled)

Cr 635 – Financial expenses (the loan interests recorded to financial expenses in this period).

– If the period from maturity date for payment of share purchase made by investors to the date on which the enterprise receives Certificate of Business registration is longer than 3 months, the enterprise may determine interests paid to investors:

+ Interests payable shall be recorded as follows:

Dr 635 – Financial expenses

Cr 335 – Accrued expenses.

+ When paying to investors, the following accounts shall be recorded as follows:

Dr 335 – Accrued expenses.

Cr 111, 112.

m) Accounting for accrued expenses for provisional determination of costs of sold property held for sale.

– When accruing expenses for provisional determination of costs of sold property held for sale, the following accounts shall be recorded as follows:

Dr 632 – Costs of goods sold

Cr 335 – Accrued expenses.

– The expenses incurred from accepted construction with sufficient documents shall be recorded to expenses incurred from property construction as follows:

Dr 154 – Work in progress

Dr 133 – Deductible VAT

Cr, relevant.

– When there are sufficient documents proving that accrued expenses actually incurs, a decrease in accrued expenses and work in progress shall be recorded as follows:

Dr 335- – Accrued expenses.

Cr 154- – Work in progress.

– When all property projects are completed, a decrease in the remaining accrued expenses shall be recorded as follows:

Dr 335- – Accrued expenses.

Cr 154- – Work in progress.

Cr 632 – Costs of goods sold (positive difference between remaining accrued expenses and actual expenses incurred).

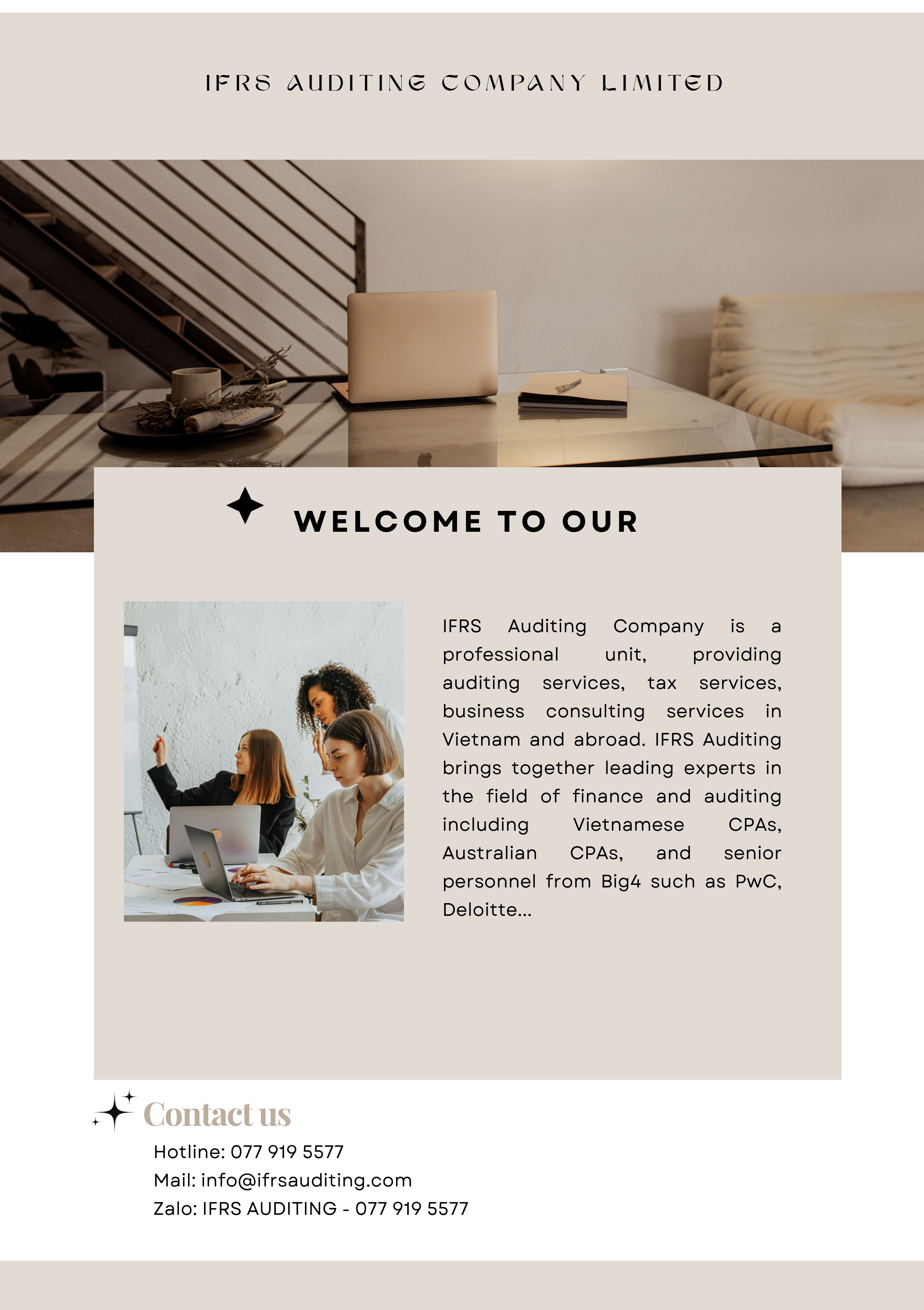

IFRS Auditing and Consulting Company Limited

The company provides a wide range of services such as audit of financial statements, tax advice, accounting services and valuation services with leading experts working in large auditing firms, multinational corporations